Zelle is the largest peer-to-peer payments network in the United States by any metric you care to slice it by. More than 120 million people are enrolled and more than $600 billion dollars cross its rails annually. In other words, 50% of the adults in the United States are Zelle users. Despite this runaway success you won’t have seen any fintech startups on there; the door has not been opened to them. Given how incredibly relevant Zelle is, the continued inability of fintechs to access it presents a major stumbling block for any new depository-account-with-debit-card type products entering the market.

Today we are excited to announce Bridge, our new product for bringing Zelle to neobanks and other types of non-bank fintech companies that issue their own debit cards and have been historically excluded from Zelle.

Despite not being a direct member of Zelle, with Bridge you can now enroll your users using the debit card PANs you’ve issued them. When a user sends money, their card is debited, and any incoming funds are immediately pushed to their card. In effect the debit card serves as both the entry and exit points to the Zelle network.

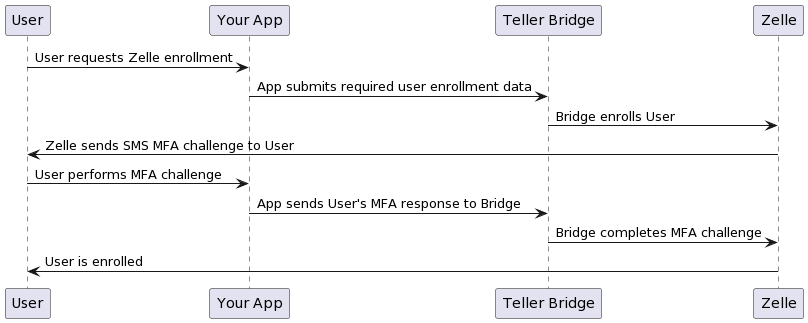

When the user requests to enroll, your app submits the required information to Bridge, which includes the telephone number or email the user wishes to register with Zelle and their card information that you as the issuer already possess. Bridge then submits all of this to Zelle, and after a simple SMS MFA challenge the user is enrolled and ready to send and receive payments.

Enrolling your users on Zelle

Once enrolled your app can send payments and create payment requests on behalf of the user, allowing you to build a fully native Zelle experience in your app as if you were a first-class participant of the Zelle scheme.

Unlock the power of Zelle with Teller Bridge.

Visit our booth at Money 2020 to find out more or contact our sales team today.

All product and company names are trademarks™ or registered trademarks® of their respective holders. Their usage does not imply any affiliation with or endorsement by their holders.